Every real estate transaction comes with a certain amount of risk. Whether you’re buying or selling, you leave

yourself open to potential issues at every stage. It can be especially difficult for homebuyers – luckily, there are

some simple ways to mitigate common risk factors and find your dream home.

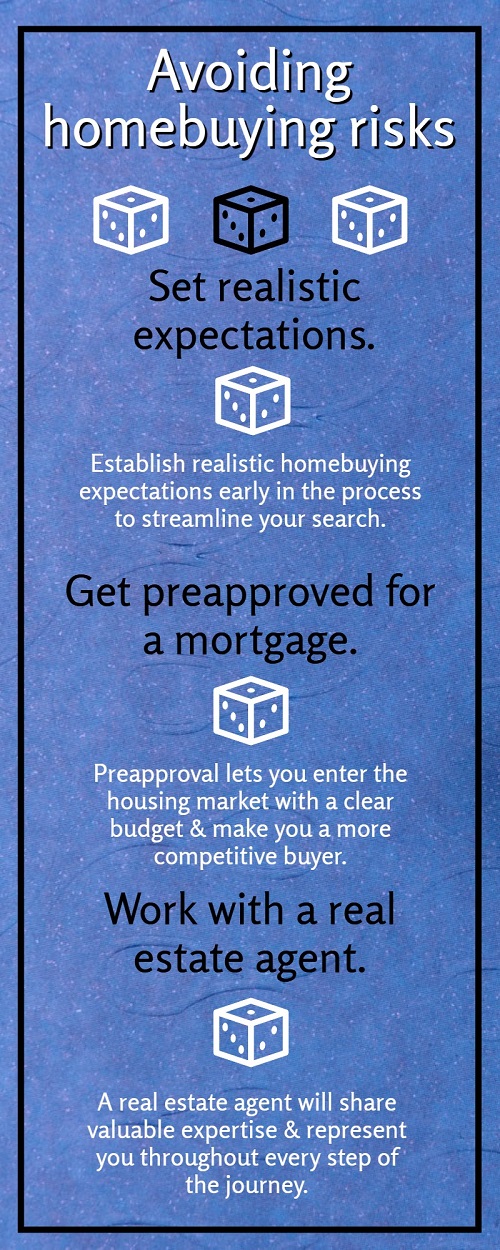

Set realistic homebuying expectations

How you search for a home may determine whether you are successful or unsuccessful. For example, if you evaluate

houses that fall outside your price range, you may struggle to find a home that you can actually afford. On the

other hand, if you establish realistic homebuying expectations from the get-go, you may be able to streamline your

house search.

Get pre-approved for a mortgage

Getting pre-approved for a mortgage is essential to avoiding multiple potential homebuying pitfalls. Pre-approval

lets you enter the housing market with a clear budget and narrow your house search accordingly. It can also give you

an advantage over competing buyers, as it shows the seller you’re financially prepared to follow through on the

sale.

Work with a real estate agent

When you hire a real estate agent to help you buy a home, you have a powerful teammate in your corner. A real

estate agent understands the housing market and can share valuable expertise and guidance on every step of the

journey. An agent will also be your legal representation, helping you navigate all the paperwork and logistics

involved.

For many, buying a home is the biggest financial decision of their lives. As such, it’s not a process to be taken

lightly. The more you can do to avoid common risks associated with homebuying, the more successful and happy you’ll

be in your new home.